-

×

Tan Choudhury - E-Com Mastery Program

2 × $47.00

Tan Choudhury - E-Com Mastery Program

2 × $47.00 -

×

Dale Sellers - Life Mastery Class 20 - The Awakening and Final Test

1 × $15.00

Dale Sellers - Life Mastery Class 20 - The Awakening and Final Test

1 × $15.00 -

×

Local Consults from Jason Fladlien & Caro McCourtie

2 × $57.00

Local Consults from Jason Fladlien & Caro McCourtie

2 × $57.00 -

×

Financial Freedom Through Blogging by Lidiya K

1 × $52.00

Financial Freedom Through Blogging by Lidiya K

1 × $52.00 -

×

Video Strategy Academy 2.0 by Trena Little

1 × $129.00

Video Strategy Academy 2.0 by Trena Little

1 × $129.00 -

×

Stephen G.Ryan - Financial Instruments & Institutions (2nd Ed.)

1 × $25.00

Stephen G.Ryan - Financial Instruments & Institutions (2nd Ed.)

1 × $25.00 -

×

RazorSocial’s – Blogging Blueprint for Success presented by Ian Cleary

4 × $57.00

RazorSocial’s – Blogging Blueprint for Success presented by Ian Cleary

4 × $57.00 -

×

The Brand Strategy Course by Bernadette Jiwa

4 × $39.00

The Brand Strategy Course by Bernadette Jiwa

4 × $39.00 -

×

BeachBody: - TurboFire Workout Complete Set by Chalene Johnson

1 × $72.00

BeachBody: - TurboFire Workout Complete Set by Chalene Johnson

1 × $72.00 -

×

Liz Benny - InstaSocial Secrets

1 × $127.00

Liz Benny - InstaSocial Secrets

1 × $127.00 -

×

Jerry Banfield with EDUfyre - Master Entrepreneurship Online

2 × $25.00

Jerry Banfield with EDUfyre - Master Entrepreneurship Online

2 × $25.00 -

×

Lillian Too - Feng Shui For Real Estate Success

1 × $97.00

Lillian Too - Feng Shui For Real Estate Success

1 × $97.00 -

×

Thinking For A Change from Michael Breen

4 × $52.00

Thinking For A Change from Michael Breen

4 × $52.00 -

×

Island Lifestyle Blueprint from Jon Tarr & Kyle Bell’s

3 × $57.00

Island Lifestyle Blueprint from Jon Tarr & Kyle Bell’s

3 × $57.00 -

×

John La Tourrette - The 18 Fighting Principles of Bruce Lee

1 × $25.00

John La Tourrette - The 18 Fighting Principles of Bruce Lee

1 × $25.00 -

×

Jeff Brown - The Enrealment Method

2 × $95.00

Jeff Brown - The Enrealment Method

2 × $95.00 -

×

Inner Bonding - Attracting Your Beloved by Margaret Paul

1 × $59.00

Inner Bonding - Attracting Your Beloved by Margaret Paul

1 × $59.00 -

×

Voice Dialogue Series by Hal and Sidra Stone

1 × $27.00

Voice Dialogue Series by Hal and Sidra Stone

1 × $27.00 -

×

Sales U from Jack Daly

1 × $137.00

Sales U from Jack Daly

1 × $137.00 -

×

Jason Capital - Jedi Mini Tricks and Dark Side Mind Tricks

1 × $32.00

Jason Capital - Jedi Mini Tricks and Dark Side Mind Tricks

1 × $32.00 -

×

Eric Thomas and Associates - Breathe University

1 × $87.00

Eric Thomas and Associates - Breathe University

1 × $87.00 -

×

Jerry Banfield with EDUfyre - How to Teach an Online Course

1 × $15.00

Jerry Banfield with EDUfyre - How to Teach an Online Course

1 × $15.00 -

×

Mike McMahon – Professional Trader Series DVD Set (Full) (tradingacademy.com)

2 × $65.00

Mike McMahon – Professional Trader Series DVD Set (Full) (tradingacademy.com)

2 × $65.00 -

×

Essentials of Tai Chi and Qigong

1 × $22.00

Essentials of Tai Chi and Qigong

1 × $22.00 -

×

Nick Van Nice & John Sheely – Master CTS Swing Trading (Video & Manual)

2 × $23.00

Nick Van Nice & John Sheely – Master CTS Swing Trading (Video & Manual)

2 × $23.00 -

×

Rize Capital - ADVANCED LEVEL - Learn NinjaScript Programming for NT8

1 × $179.00

Rize Capital - ADVANCED LEVEL - Learn NinjaScript Programming for NT8

1 × $179.00 -

×

The Fence by Geoff Thompson

1 × $29.00

The Fence by Geoff Thompson

1 × $29.00 -

×

Joint Venture Equity vs. Fund Structures™

1 × $142.00

Joint Venture Equity vs. Fund Structures™

1 × $142.00 -

×

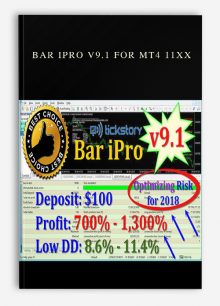

Bar Ipro v9.1 for MT4 11XX

1 × $49.00

Bar Ipro v9.1 for MT4 11XX

1 × $49.00 -

×

John La Tourrette - Secrets of Pure Hakalau Prime & Time Distortion

1 × $19.00

John La Tourrette - Secrets of Pure Hakalau Prime & Time Distortion

1 × $19.00 -

×

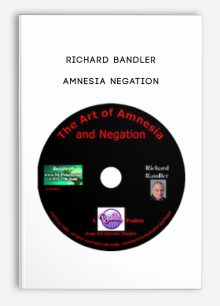

Amnesia Negation by Richard Bandler

1 × $19.00

Amnesia Negation by Richard Bandler

1 × $19.00 -

×

International Marketing Foundations

3 × $15.00

International Marketing Foundations

3 × $15.00 -

×

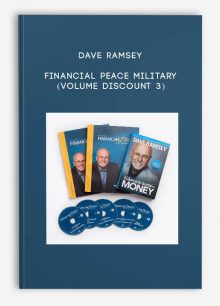

Dave Ramsey - Financial Peace Military (Volume Discount 3)

1 × $199.00

Dave Ramsey - Financial Peace Military (Volume Discount 3)

1 × $199.00 -

×

Meetup Master 2.0 presented by Mel Cutler

4 × $47.00

Meetup Master 2.0 presented by Mel Cutler

4 × $47.00 -

×

Lead Selling Machine by Ron LeGrand

1 × $57.00

Lead Selling Machine by Ron LeGrand

1 × $57.00 -

×

Pristine – Oliver Velez & Greg Capra – Trading the Pristine Method. The Refresher Course – I & II

2 × $39.00

Pristine – Oliver Velez & Greg Capra – Trading the Pristine Method. The Refresher Course – I & II

2 × $39.00 -

×

Dr. Steven Farmer – The 5 Ancestral Realms

1 × $89.00

Dr. Steven Farmer – The 5 Ancestral Realms

1 × $89.00 -

×

Lawrence Bernstein – The BIG Idea Health Swipes

1 × $57.00

Lawrence Bernstein – The BIG Idea Health Swipes

1 × $57.00 -

×

NLP Language Guru from Michael Breen

4 × $52.00

NLP Language Guru from Michael Breen

4 × $52.00 -

×

SOT Advanced Course (May 2014)

2 × $72.00

SOT Advanced Course (May 2014)

2 × $72.00 -

×

Online Marketing Classroom 2019 by Steven Clayton & Aidan Booth

1 × $147.00

Online Marketing Classroom 2019 by Steven Clayton & Aidan Booth

1 × $147.00 -

×

Marisa Peer – Freedom From Drugs

1 × $17.00

Marisa Peer – Freedom From Drugs

1 × $17.00 -

×

Online Seminar Beyond Basics One, Two and Three 2007 by Markay Latimer

1 × $88.00

Online Seminar Beyond Basics One, Two and Three 2007 by Markay Latimer

1 × $88.00 -

×

Quieting The Mind (1994) by Helen Palmer

1 × $19.00

Quieting The Mind (1994) by Helen Palmer

1 × $19.00 -

×

Music Theory for Electronic Music COMPLETE: Parts 1, 2, & 3

1 × $42.00

Music Theory for Electronic Music COMPLETE: Parts 1, 2, & 3

1 × $42.00 -

×

Piptronic Robot

1 × $25.00

Piptronic Robot

1 × $25.00 -

×

Pristine – Oliver Velez – Core, Swing, Guerrilla, Momentum Trading, Micro Trading Tactics

4 × $59.00

Pristine – Oliver Velez – Core, Swing, Guerrilla, Momentum Trading, Micro Trading Tactics

4 × $59.00 -

×

VSA Stocks, Commodities and Options Trading

1 × $139.00

VSA Stocks, Commodities and Options Trading

1 × $139.00 -

×

Paul Lemal – Bottom Springers. Bonsai Elite WaveTrader Course (8 DVDs & Manuals)

2 × $33.00

Paul Lemal – Bottom Springers. Bonsai Elite WaveTrader Course (8 DVDs & Manuals)

2 × $33.00 -

×

The Ultimate Marketing Machine from Dave Dee

2 × $127.00

The Ultimate Marketing Machine from Dave Dee

2 × $127.00 -

×

Online Dream Coach Certification presented by Marcia Wieder

3 × $41.00

Online Dream Coach Certification presented by Marcia Wieder

3 × $41.00 -

×

Water Bears No Scars - Japanese Lifeways for Personal Growth by David K. Reynolds

1 × $35.00

Water Bears No Scars - Japanese Lifeways for Personal Growth by David K. Reynolds

1 × $35.00 -

×

Robin Sharma – The Titan Academy 4

1 × $92.00

Robin Sharma – The Titan Academy 4

1 × $92.00 -

×

Ehab Masoud - Happiness Daily Boost by simple PROVEN steps

1 × $59.00

Ehab Masoud - Happiness Daily Boost by simple PROVEN steps

1 × $59.00 -

×

Carlos Xuma - Get a Girlfriend FAST

1 × $37.00

Carlos Xuma - Get a Girlfriend FAST

1 × $37.00 -

×

Deja vu by Arash Dibazar

1 × $59.00

Deja vu by Arash Dibazar

1 × $59.00 -

×

Barrington McIntosh - International Selling Mastermind

1 × $47.00

Barrington McIntosh - International Selling Mastermind

1 × $47.00 -

×

William Bronchick - The Legalwiz Guide to Lease Options

1 × $62.00

William Bronchick - The Legalwiz Guide to Lease Options

1 × $62.00 -

×

The Art of Advanced Listening by Rob McNamara

1 × $27.00

The Art of Advanced Listening by Rob McNamara

1 × $27.00 -

×

Kyokushin karate Katas

1 × $29.90

Kyokushin karate Katas

1 × $29.90 -

×

Billy Gene – Behind The Geneius Workshop Recording

1 × $42.00

Billy Gene – Behind The Geneius Workshop Recording

1 × $42.00 -

×

TradeGuider Education Package

1 × $179.00

TradeGuider Education Package

1 × $179.00 -

×

ADVANCED TRADITIONAL SWORD SERIES TITLES | Digital Download

1 × $29.00

ADVANCED TRADITIONAL SWORD SERIES TITLES | Digital Download

1 × $29.00 -

×

THE HOOK CHECKLIST by Friedemann Findeisen

5 × $25.00

THE HOOK CHECKLIST by Friedemann Findeisen

5 × $25.00 -

×

Even More Complete Shoulder & Hip Blueprint: version 2.0 by Tony Gentilcore & Dean Somerset

1 × $47.00

Even More Complete Shoulder & Hip Blueprint: version 2.0 by Tony Gentilcore & Dean Somerset

1 × $47.00 -

×

Authority Marketer from Kim Klaver

5 × $47.00

Authority Marketer from Kim Klaver

5 × $47.00 -

×

Jeff Sauer – FB Ads Complete Data Master Package

1 × $119.00

Jeff Sauer – FB Ads Complete Data Master Package

1 × $119.00 -

×

Ordinary Guys Monthly Programme by Timur Smirnov

1 × $67.00

Ordinary Guys Monthly Programme by Timur Smirnov

1 × $67.00 -

×

Amber Lilyestrom - Beautiful Brand - Beautiful You

1 × $57.00

Amber Lilyestrom - Beautiful Brand - Beautiful You

1 × $57.00 -

×

Steve Larsen - Offermind 2021 Replays

1 × $57.00

Steve Larsen - Offermind 2021 Replays

1 × $57.00 -

×

Lewis Howes - Unleash Your Greatness Summit 2015

1 × $29.00

Lewis Howes - Unleash Your Greatness Summit 2015

1 × $29.00 -

×

Alex Loyd – Immune System Master Key

1 × $47.00

Alex Loyd – Immune System Master Key

1 × $47.00 -

×

BRIAN DAVID PHILLIPS ADVANCED EROTIC HYPNOSIS

1 × $42.00

BRIAN DAVID PHILLIPS ADVANCED EROTIC HYPNOSIS

1 × $42.00 -

×

Stephanie Fields & The RevU Teamv - Revolution U

1 × $87.00

Stephanie Fields & The RevU Teamv - Revolution U

1 × $87.00 -

×

Joey Yap – Real Feng Shui

1 × $97.00

Joey Yap – Real Feng Shui

1 × $97.00 -

×

Kody Knows – Native Mastery

1 × $299.00

Kody Knows – Native Mastery

1 × $299.00 -

×

Photographing Montana Big Skies

1 × $15.00

Photographing Montana Big Skies

1 × $15.00 -

×

Doña Eugenia Pineda Casimiro - The Healing Potential of Sacred Mushrooms

1 × $95.00

Doña Eugenia Pineda Casimiro - The Healing Potential of Sacred Mushrooms

1 × $95.00 -

×

Complete Fascinate System for Busines from Sally Hogshead

2 × $137.00

Complete Fascinate System for Busines from Sally Hogshead

2 × $137.00 -

×

Gina Devee - Men and Money course

1 × $47.00

Gina Devee - Men and Money course

1 × $47.00 -

×

Membership Arbitrage from Ben Adkins’

1 × $37.00

Membership Arbitrage from Ben Adkins’

1 × $37.00 -

×

Shapeshifting Your Reality by John Perkins

1 × $87.00

Shapeshifting Your Reality by John Perkins

1 × $87.00 -

×

[10] Ultimate 120 Courses - Jerry Banfield Bundle

1 × $2,399.00

[10] Ultimate 120 Courses - Jerry Banfield Bundle

1 × $2,399.00 -

×

Early Interventions Social-Emotional, Sensory from Karen Lea Hyche

1 × $59.00

Early Interventions Social-Emotional, Sensory from Karen Lea Hyche

1 × $59.00 -

×

Ethical Principles in the Practice of North Carolina Mental Health Professionals from Allan M. Tepper

1 × $32.00

Ethical Principles in the Practice of North Carolina Mental Health Professionals from Allan M. Tepper

1 × $32.00 -

×

Gracie Barra - Syllabus

1 × $32.00

Gracie Barra - Syllabus

1 × $32.00 -

×

Stuart Lichtman SSPT 1 COMPLETE (Weeks 1 -18 + BONUSES)

1 × $199.00

Stuart Lichtman SSPT 1 COMPLETE (Weeks 1 -18 + BONUSES)

1 × $199.00 -

×

Josh Harding - 17 Innocent Words that Make Her Horny - Erect on Demand GB

1 × $29.00

Josh Harding - 17 Innocent Words that Make Her Horny - Erect on Demand GB

1 × $29.00 -

×

Tony Robbins – Ultimate Edge

1 × $32.00

Tony Robbins – Ultimate Edge

1 × $32.00 -

×

VectorVest - Seven Secrets to Making Money with VectorVest

1 × $10.00

VectorVest - Seven Secrets to Making Money with VectorVest

1 × $10.00 -

×

Richard Clear - Combat Tai Chi vol 17 - Breathing for Tai Chi

3 × $47.00

Richard Clear - Combat Tai Chi vol 17 - Breathing for Tai Chi

3 × $47.00 -

×

Christine Stevens - 7 Scales for the Native American Flute to Create Joy, Musical Magic & Spiritual Growth

1 × $95.00

Christine Stevens - 7 Scales for the Native American Flute to Create Joy, Musical Magic & Spiritual Growth

1 × $95.00 -

×

Affiliate Formula X – Affiliate Training presented by Sarah Staar

3 × $37.00

Affiliate Formula X – Affiliate Training presented by Sarah Staar

3 × $37.00 -

×

Feed A Starving Crowd Course from Robert Coorey

3 × $39.00

Feed A Starving Crowd Course from Robert Coorey

3 × $39.00 -

×

Kam Yuen – Speciality Course 1-3 Bundle: Complete Speciality Training Package

1 × $189.00

Kam Yuen – Speciality Course 1-3 Bundle: Complete Speciality Training Package

1 × $189.00 -

×

Jon Mac - The Millionaire Challenge 2.0

1 × $247.00

Jon Mac - The Millionaire Challenge 2.0

1 × $247.00 -

×

Eric L. Ball - Sustained by Eating, Consumed by Eating Right: Reflections, Rhymes, Rants, and Recipes (2013)

1 × $12.00

Eric L. Ball - Sustained by Eating, Consumed by Eating Right: Reflections, Rhymes, Rants, and Recipes (2013)

1 × $12.00 -

×

SWIS Video Flix Library - Rehabilitation

1 × $27.00

SWIS Video Flix Library - Rehabilitation

1 × $27.00 -

×

Deepak Chopra - SynchroDestiny Course

1 × $57.00

Deepak Chopra - SynchroDestiny Course

1 × $57.00 -

×

K.P. Khalsa - The Path of Ayurvedic Herbalism

3 × $95.00

K.P. Khalsa - The Path of Ayurvedic Herbalism

3 × $95.00 -

×

For Him: Knowing Your Truth to Open Her Heart by David Deida

1 × $22.00

For Him: Knowing Your Truth to Open Her Heart by David Deida

1 × $22.00 -

×

Earn More Writing PRO Platinum Bundle

4 × $79.00

Earn More Writing PRO Platinum Bundle

4 × $79.00 -

×

Garrett Gunderson - Wealth Factory

1 × $57.00

Garrett Gunderson - Wealth Factory

1 × $57.00 -

×

GANNacci Code Elite + Training Course

2 × $92.00

GANNacci Code Elite + Training Course

2 × $92.00 -

×

SELF STORAGE CASH FLOW from Monica Main

1 × $52.00

SELF STORAGE CASH FLOW from Monica Main

1 × $52.00 -

×

Darren Hanser - The Entire Email Profits Boot Camp

2 × $47.00

Darren Hanser - The Entire Email Profits Boot Camp

2 × $47.00 -

×

![Copy Hackers [Joanna Wiebe] – Email Copywriting](https://tradersoffer.forex/wp-content/uploads/2017/02/Copy-Hackers-Joanna-Wiebe-–-Email-Copywriting-220x306.jpg) Email Copywriting from Copy Hackers [Joanna Wiebe]

3 × $47.00

Email Copywriting from Copy Hackers [Joanna Wiebe]

3 × $47.00 -

×

Frank Kern - Screw Google System

1 × $52.00

Frank Kern - Screw Google System

1 × $52.00 -

×

Two Simple Setups For All Markets (Parts 1, 2, 3) from Rob Hoffman

1 × $75.00

Two Simple Setups For All Markets (Parts 1, 2, 3) from Rob Hoffman

1 × $75.00 -

×

Pablo Farías Navarro - Learn Web Development by Creating a Social Network

1 × $32.00

Pablo Farías Navarro - Learn Web Development by Creating a Social Network

1 × $32.00 -

×

ITPM - Emergency Room

1 × $97.00

ITPM - Emergency Room

1 × $97.00 -

×

Opening Your Third Eye from Raja Choudhury

2 × $87.00

Opening Your Third Eye from Raja Choudhury

2 × $87.00 -

×

MLS Domination presented by Jim Huntzicker

2 × $87.00

MLS Domination presented by Jim Huntzicker

2 × $87.00 -

×

Diamond Consciousness in Relationships Activation - Diamond Energy by Jacqueline Joy

1 × $31.10

Diamond Consciousness in Relationships Activation - Diamond Energy by Jacqueline Joy

1 × $31.10 -

×

The X24 Subliminal Audio Aphrodisiac by Subliminal Shop

1 × $32.00

The X24 Subliminal Audio Aphrodisiac by Subliminal Shop

1 × $32.00 -

×

David Bean – Cobra (aka Viper Crude)

1 × $69.00

David Bean – Cobra (aka Viper Crude)

1 × $69.00 -

×

Heart and Lung Sounds, 2nd Edition from Cyndi Zarbano

1 × $17.00

Heart and Lung Sounds, 2nd Edition from Cyndi Zarbano

1 × $17.00 -

×

SMALL DRAGON PREMIUM 2.0

1 × $549.00

SMALL DRAGON PREMIUM 2.0

1 × $549.00 -

×

60 Years of challenge - Even Faster Lays

1 × $27.00

60 Years of challenge - Even Faster Lays

1 × $27.00 -

×

Double Your Income and Your Time Off from Ryan Eliason

3 × $87.00

Double Your Income and Your Time Off from Ryan Eliason

3 × $87.00 -

×

insider Internet Dating by Dave M

1 × $19.00

insider Internet Dating by Dave M

1 × $19.00 -

×

Joe Ross Trading All Markets Recorded Webinar

1 × $189.00

Joe Ross Trading All Markets Recorded Webinar

1 × $189.00 -

×

Playboy Italy - May 2010

2 × $10.00

Playboy Italy - May 2010

2 × $10.00 -

×

Pleasure Proof Your Relationship

1 × $147.00

Pleasure Proof Your Relationship

1 × $147.00 -

×

Jim Cockrum – CES Conference 2014

1 × $67.00

Jim Cockrum – CES Conference 2014

1 × $67.00 -

×

Edward De Bono - Effective Thinking & CoRT Thinking

1 × $89.00

Edward De Bono - Effective Thinking & CoRT Thinking

1 × $89.00 -

×

MTI – Trend Trader Course (Feb 2014)

1 × $59.00

MTI – Trend Trader Course (Feb 2014)

1 × $59.00 -

×

J. S. Epperson - Higher ~ Deep Theta Meditation (2012 Edition)

1 × $29.00

J. S. Epperson - Higher ~ Deep Theta Meditation (2012 Edition)

1 × $29.00 -

×

Dirk Zeller - Team Mastery

2 × $57.00

Dirk Zeller - Team Mastery

2 × $57.00 -

×

Unlimited Lover from David Snyder

1 × $67.00

Unlimited Lover from David Snyder

1 × $67.00 -

×

Arash Dibazar - Dragon Heart, Ignite The Fire

1 × $62.00

Arash Dibazar - Dragon Heart, Ignite The Fire

1 × $62.00 -

×

Danny Kavadlo & Al Kavadlo - Get Strong, The Ultimate 16-Week Transformation Program For Gaining Muscle And Strength

1 × $15.00

Danny Kavadlo & Al Kavadlo - Get Strong, The Ultimate 16-Week Transformation Program For Gaining Muscle And Strength

1 × $15.00 -

×

Dr. Stephen E. West - The Golden 7 Plus Two (The Art of Lymphasizing)

1 × $19.00

Dr. Stephen E. West - The Golden 7 Plus Two (The Art of Lymphasizing)

1 × $19.00 -

×

Duston McGroarty - Affiliate Ground Zero

1 × $59.00

Duston McGroarty - Affiliate Ground Zero

1 × $59.00 -

×

Dan DaSilva - $100K Blueprint : 8 Week Shopify Training Program

1 × $92.00

Dan DaSilva - $100K Blueprint : 8 Week Shopify Training Program

1 × $92.00 -

×

Jerry Banfield with EDUfyre - GRE Vocabulary - increase your GRE Verbal score

2 × $12.00

Jerry Banfield with EDUfyre - GRE Vocabulary - increase your GRE Verbal score

2 × $12.00 -

×

Julie Ball – Subscription Box Bootcamp

2 × $27.00

Julie Ball – Subscription Box Bootcamp

2 × $27.00 -

×

Chris Scott – Real Estate Digital Marketer (REDM) Certification Course

1 × $55.00

Chris Scott – Real Estate Digital Marketer (REDM) Certification Course

1 × $55.00 -

×

Gustavo Gasperin - The Ace Of Escapes

2 × $27.00

Gustavo Gasperin - The Ace Of Escapes

2 × $27.00 -

×

Russell Brunson – 2 Comma Club Coaching – Home Study Course

1 × $35.00

Russell Brunson – 2 Comma Club Coaching – Home Study Course

1 × $35.00 -

×

Internal Family Systems Therapy (IFS) and Parenting - FRANK ANDERSON (Digital Seminar)

1 × $65.00

Internal Family Systems Therapy (IFS) and Parenting - FRANK ANDERSON (Digital Seminar)

1 × $65.00 -

×

Langston Kahn - Reconnect to a Sensuous World

3 × $65.00

Langston Kahn - Reconnect to a Sensuous World

3 × $65.00 -

×

Brian David Phillips - Elman - Phillips Induction

1 × $55.00

Brian David Phillips - Elman - Phillips Induction

1 × $55.00 -

×

Local Income System from Hershy

1 × $92.00

Local Income System from Hershy

1 × $92.00 -

×

Creating the Impossible by Michael Neill

1 × $19.90

Creating the Impossible by Michael Neill

1 × $19.90 -

×

DAN KENNEDY - MAXIMUM PROFITS ONLINE AND OFFLINE TRAINING

1 × $99.00

DAN KENNEDY - MAXIMUM PROFITS ONLINE AND OFFLINE TRAINING

1 × $99.00 -

×

William Bronchick - IRA Investing Advanced eCourse

1 × $42.00

William Bronchick - IRA Investing Advanced eCourse

1 × $42.00 -

×

Time of Your Life Summary Cards by Anthony Robbins

2 × $15.00

Time of Your Life Summary Cards by Anthony Robbins

2 × $15.00 -

×

The Perfect Body Course by Kristopher Dillard

1 × $77.00

The Perfect Body Course by Kristopher Dillard

1 × $77.00 -

×

7 Second Seduction + Bonuses by David Wygant

1 × $29.90

7 Second Seduction + Bonuses by David Wygant

1 × $29.90 -

×

Options Trading. The Hidden Reality Course from Charles Cottle

1 × $9.00

Options Trading. The Hidden Reality Course from Charles Cottle

1 × $9.00 -

×

Amp’d Up Podcasting by Pat Flynn

1 × $89.00

Amp’d Up Podcasting by Pat Flynn

1 × $89.00 -

×

William Bronchick – Fix and Flip/Buy and Hold Bundle

1 × $199.00

William Bronchick – Fix and Flip/Buy and Hold Bundle

1 × $199.00 -

×

Total Beaxst by Athlean X

1 × $37.00

Total Beaxst by Athlean X

1 × $37.00 -

×

High School Strength & Conditioning Coach Certification

1 × $52.00

High School Strength & Conditioning Coach Certification

1 × $52.00 -

×

Body Pump 61 by Les Mills

1 × $29.90

Body Pump 61 by Les Mills

1 × $29.90 -

×

Rize Capital - Learn NinjaScript Programming for NT8

1 × $129.00

Rize Capital - Learn NinjaScript Programming for NT8

1 × $129.00 -

×

Smart Real Estate Coach – The 31-Day Billionaire

1 × $179.00

Smart Real Estate Coach – The 31-Day Billionaire

1 × $179.00 -

×

RiskDoctor RD1 – Introduction to Options Trading the RiskDoctor Way from Charles Cottle

1 × $19.00

RiskDoctor RD1 – Introduction to Options Trading the RiskDoctor Way from Charles Cottle

1 × $19.00 -

×

David Crow - Floracopeia - Aromatherapy Foundations Certification Course

1 × $77.00

David Crow - Floracopeia - Aromatherapy Foundations Certification Course

1 × $77.00 -

×

Self-Regulation in Children from Varleisha Gibbs

1 × $32.00

Self-Regulation in Children from Varleisha Gibbs

1 × $32.00 -

×

Captain Jack - Goal Clearing Transcript

1 × $25.00

Captain Jack - Goal Clearing Transcript

1 × $25.00 -

×

Become Mr. Right by David DeAngelo

1 × $19.00

Become Mr. Right by David DeAngelo

1 × $19.00 -

×

ConversionXL, Simo Ahava - Advanced GTM

1 × $142.00

ConversionXL, Simo Ahava - Advanced GTM

1 × $142.00 -

×

Leigh Spusta - iAwake - The Teachings of Wan-Tsu Lesson 1

1 × $12.00

Leigh Spusta - iAwake - The Teachings of Wan-Tsu Lesson 1

1 × $12.00 -

×

Brian Tracy - How To Write And Become A Published Author

1 × $497.00

Brian Tracy - How To Write And Become A Published Author

1 × $497.00 -

×

Jason Linett – Hypnotize Business Boot Camp

2 × $67.00

Jason Linett – Hypnotize Business Boot Camp

2 × $67.00 -

×

John Ruskan - Emotional Clearing - Desert Dawn CD

1 × $29.00

John Ruskan - Emotional Clearing - Desert Dawn CD

1 × $29.00 -

×

Stephen Cabral – Smart Studio Systems

1 × $77.00

Stephen Cabral – Smart Studio Systems

1 × $77.00 -

×

MAM EA (Unlocked)

1 × $99.00

MAM EA (Unlocked)

1 × $99.00 -

×

Dim Mak Secrets 7 DVD set

1 × $62.00

Dim Mak Secrets 7 DVD set

1 × $62.00 -

×

BIG DRAGON PREMIUM 2.0

1 × $549.00

BIG DRAGON PREMIUM 2.0

1 × $549.00 -

×

Quantum Hypnosis Healing Personal MP3 by Talmadge Harper

1 × $37.00

Quantum Hypnosis Healing Personal MP3 by Talmadge Harper

1 × $37.00 -

×

Market Place POD Profits Xmas Package (Copy)

3 × $42.00

Market Place POD Profits Xmas Package (Copy)

3 × $42.00 -

×

Hector Castillo - King of College

2 × $25.00

Hector Castillo - King of College

2 × $25.00 -

×

Jeffrey Kennedy – 5 Basic Elliott Wave Patterns + Technical Tools

1 × $39.00

Jeffrey Kennedy – 5 Basic Elliott Wave Patterns + Technical Tools

1 × $39.00 -

×

Balance Dynamics Video Course from Michael Parsons

1 × $47.00

Balance Dynamics Video Course from Michael Parsons

1 × $47.00 -

×

DREAM GATES by Robert Moss

1 × $12.00

DREAM GATES by Robert Moss

1 × $12.00 -

×

AB Level Black - Alex Becker

2 × $225.00

AB Level Black - Alex Becker

2 × $225.00 -

×

Weight Loss - Loving Yourself by Sound Healing Center

1 × $12.00

Weight Loss - Loving Yourself by Sound Healing Center

1 × $12.00 -

×

Property Umbrella Blueprint from Jamel Gibb

1 × $57.00

Property Umbrella Blueprint from Jamel Gibb

1 × $57.00 -

×

Magic Guard Passing by Travis Stevens

1 × $17.00

Magic Guard Passing by Travis Stevens

1 × $17.00 -

×

Jack Korbid - The Secret Sex Code

1 × $19.00

Jack Korbid - The Secret Sex Code

1 × $19.00 -

×

Abby Lentz - Heavyweight Yoga: Yoga for the Body You Have Today

1 × $14.90

Abby Lentz - Heavyweight Yoga: Yoga for the Body You Have Today

1 × $14.90 -

×

Lance Edward – Raising Private Money Home Study System 2.0

1 × $77.00

Lance Edward – Raising Private Money Home Study System 2.0

1 × $77.00 -

×

A Whole New Way of Thinking About Changing Your Life by Michael Neill

1 × $12.00

A Whole New Way of Thinking About Changing Your Life by Michael Neill

1 × $12.00 -

×

Dandrew Media - Preferred Equity Financier

1 × $92.00

Dandrew Media - Preferred Equity Financier

1 × $92.00 -

×

GEOFF THOMPSON – REAL PUNCHING | Digital Download

1 × $29.00

GEOFF THOMPSON – REAL PUNCHING | Digital Download

1 × $29.00 -

×

Cinematic Music: The Essentials by Walid Feghali

1 × $35.00

Cinematic Music: The Essentials by Walid Feghali

1 × $35.00 -

×

Persuasion Enhancement Mastery System from Michael Bernoff

1 × $47.00

Persuasion Enhancement Mastery System from Michael Bernoff

1 × $47.00 -

×

Distressed Commercial RE Triage Live from Dandrew Media

1 × $142.00

Distressed Commercial RE Triage Live from Dandrew Media

1 × $142.00 -

×

Andrea De La Torre - Baby, We're Home! Now Let's Sleep

2 × $25.00

Andrea De La Torre - Baby, We're Home! Now Let's Sleep

2 × $25.00 -

×

Contextual Hypnotherapy – Evidenced Based Approaches

3 × $47.00

Contextual Hypnotherapy – Evidenced Based Approaches

3 × $47.00 -

×

SPIRITUALITY BEYOND RELIGION by Lionel Corbett

1 × $12.00

SPIRITUALITY BEYOND RELIGION by Lionel Corbett

1 × $12.00 -

×

William Bronchick - Advanced Ultimate Guide to Wholesaling Houses

1 × $62.00

William Bronchick - Advanced Ultimate Guide to Wholesaling Houses

1 × $62.00 -

×

Ezra Firestone - Blue Ribbon Mastermind

1 × $499.00

Ezra Firestone - Blue Ribbon Mastermind

1 × $499.00 -

×

The Hidden Vortex from Arash Dibazar

1 × $47.00

The Hidden Vortex from Arash Dibazar

1 × $47.00 -

×

IBD’s Level 3 – Chart School

2 × $99.00

IBD’s Level 3 – Chart School

2 × $99.00 -

×

Hilary Crowley - Befriend Your Intuition

1 × $95.00

Hilary Crowley - Befriend Your Intuition

1 × $95.00 -

×

Montessori Math Course (Early Childhood and Elementary) montessori materials montessori toys early learning kids books

1 × $49.00

Montessori Math Course (Early Childhood and Elementary) montessori materials montessori toys early learning kids books

1 × $49.00 -

×

Carb-Loaded-A Culture Dying to Eat (2014)

2 × $42.00

Carb-Loaded-A Culture Dying to Eat (2014)

2 × $42.00 -

×

Magnetic Memory Method Podcast - Anthony Metivier

1 × $47.00

Magnetic Memory Method Podcast - Anthony Metivier

1 × $47.00 -

×

Tom O’Connor NLP – Task Decomposition The “Magic Power of Goal Getters”

1 × $52.00

Tom O’Connor NLP – Task Decomposition The “Magic Power of Goal Getters”

1 × $52.00 -

×

Dementia and the Aging Brain from ROY D. STEINBERG, Peter R. Johnson, John Arden

1 × $59.00

Dementia and the Aging Brain from ROY D. STEINBERG, Peter R. Johnson, John Arden

1 × $59.00 -

×

ALL ABOUT COMPOSITION by Kirsten Lewis

2 × $79.00

ALL ABOUT COMPOSITION by Kirsten Lewis

2 × $79.00 -

×

Lee Gettess’s Package

1 × $57.00

Lee Gettess’s Package

1 × $57.00 -

×

A Game Plan for Investing in the 21st Century by Thomas J.Dorsey

1 × $25.00

A Game Plan for Investing in the 21st Century by Thomas J.Dorsey

1 × $25.00 -

×

Annual 2016 Chakra Activation & Clearing Session - Kairos by Carol Tuttle

1 × $29.00

Annual 2016 Chakra Activation & Clearing Session - Kairos by Carol Tuttle

1 × $29.00 -

×

David Snyder - Conversational Persuasion & Influence

1 × $47.00

David Snyder - Conversational Persuasion & Influence

1 × $47.00 -

×

Geriatric Emergencies from Steven Atkinson

1 × $17.00

Geriatric Emergencies from Steven Atkinson

1 × $17.00 -

×

Judy Rees - X-Ray Listener - The Metaphor Mastery Programme

2 × $57.00

Judy Rees - X-Ray Listener - The Metaphor Mastery Programme

2 × $57.00 -

×

Jerry Banfield with EDUfyre - The Complete YouTube Course: Go from Beginner to Advanced

1 × $59.00

Jerry Banfield with EDUfyre - The Complete YouTube Course: Go from Beginner to Advanced

1 × $59.00 -

×

Tak Wah Eng – Tiger Claw Kung Fu Series (Vol.1,2,5,6)

1 × $32.00

Tak Wah Eng – Tiger Claw Kung Fu Series (Vol.1,2,5,6)

1 × $32.00 -

×

The Soul Evolution Intensive by Linda Backman

1 × $89.00

The Soul Evolution Intensive by Linda Backman

1 × $89.00 -

×

Increase Your Prosperity from Art Giser

1 × $25.00

Increase Your Prosperity from Art Giser

1 × $25.00 -

×

SEO Basics by Rachel Paul

1 × $25.00

SEO Basics by Rachel Paul

1 × $25.00 -

×

David F.Ruccio - Economic Representations

1 × $15.00

David F.Ruccio - Economic Representations

1 × $15.00 -

×

Kirill Eremenko - Debugging and Testing Android Applications Training Video

1 × $52.00

Kirill Eremenko - Debugging and Testing Android Applications Training Video

1 × $52.00 -

×

Michael Parsons – Reversal Magic Video Course

1 × $37.00

Michael Parsons – Reversal Magic Video Course

1 × $37.00 -

×

Product Launch Group Coaching from Kevin Fahey

1 × $62.00

Product Launch Group Coaching from Kevin Fahey

1 × $62.00 -

×

Darlene Nelson Powell MEGA DVD BUNDLE From BetterTrades

1 × $588.00

Darlene Nelson Powell MEGA DVD BUNDLE From BetterTrades

1 × $588.00 -

×

Technical Timing Patterns – David Elliott

1 × $77.00

Technical Timing Patterns – David Elliott

1 × $77.00 -

×

Sergio Magaña - The Toltec Secrets of Dreaming

1 × $75.00

Sergio Magaña - The Toltec Secrets of Dreaming

1 × $75.00 -

×

Champion Performance Specialist from Mike Reinold

1 × $127.00

Champion Performance Specialist from Mike Reinold

1 × $127.00 -

×

Fire Your Financial Advisor! by James M. Dahle, MD, FACEP

1 × $99.00

Fire Your Financial Advisor! by James M. Dahle, MD, FACEP

1 × $99.00 -

×

Attachment and the Dance of Sex from Susan Johnson

1 × $17.00

Attachment and the Dance of Sex from Susan Johnson

1 × $17.00 -

×

Michael Senoff – Instant Contract Agreement Guide

1 × $27.00

Michael Senoff – Instant Contract Agreement Guide

1 × $27.00 -

×

YIN Force Activator by Rudy Hunter

1 × $32.00

YIN Force Activator by Rudy Hunter

1 × $32.00 -

×

The Inflection Point Revised Edition by Charlie Burton

1 × $122.00

The Inflection Point Revised Edition by Charlie Burton

1 × $122.00 -

×

Launch Grid 2016 from Ryan Deiss (Digital Marketer)

1 × $67.00

Launch Grid 2016 from Ryan Deiss (Digital Marketer)

1 × $67.00 -

×

Quantifycapital - Quantitative Trading Program

1 × $165.00

Quantifycapital - Quantitative Trading Program

1 × $165.00 -

×

Vincent Dignan - Christmas Bundle + Secret Sauce: The Ultimate Growth Hacking Guide

1 × $47.00

Vincent Dignan - Christmas Bundle + Secret Sauce: The Ultimate Growth Hacking Guide

1 × $47.00 -

×

Zach & Jody - The Harvest Workshop

1 × $52.00

Zach & Jody - The Harvest Workshop

1 × $52.00 -

×

Advanced Price Action (TWE) (Oct 2013)

1 × $65.00

Advanced Price Action (TWE) (Oct 2013)

1 × $65.00 -

×

Business Builder Mastery from Jaelin White

2 × $197.00

Business Builder Mastery from Jaelin White

2 × $197.00 -

×

Arash Dibazar - State Of Mind

1 × $42.00

Arash Dibazar - State Of Mind

1 × $42.00 -

×

Live Lecture 18th November 2017 by Arash Dibazar

1 × $59.00

Live Lecture 18th November 2017 by Arash Dibazar

1 × $59.00 -

×

Myles Wilson Walker - The Power of the Hexagon (Complete Course)

1 × $19.00

Myles Wilson Walker - The Power of the Hexagon (Complete Course)

1 × $19.00 -

×

Edward Hayes – Facebook Ads Funnel For Wholesale Real Estate Bundle

1 × $65.00

Edward Hayes – Facebook Ads Funnel For Wholesale Real Estate Bundle

1 × $65.00 -

×

Tube PowerHouse 2.0 from Jon Penberthy

1 × $37.00

Tube PowerHouse 2.0 from Jon Penberthy

1 × $37.00 -

×

Fox Scalper

1 × $35.00

Fox Scalper

1 × $35.00 -

×

Gokce Capital – Gokce Land Investing Program

1 × $135.00

Gokce Capital – Gokce Land Investing Program

1 × $135.00 -

×

Wendy Patton – Investing in Real Estate With Lease Options and “Subject-To” Deals

1 × $9.00

Wendy Patton – Investing in Real Estate With Lease Options and “Subject-To” Deals

1 × $9.00 -

×

Dan Gibby Seminar Series – 3 DVD

1 × $39.00

Dan Gibby Seminar Series – 3 DVD

1 × $39.00 -

×

The Agency Sales System from Andrew Dymski

1 × $137.00

The Agency Sales System from Andrew Dymski

1 × $137.00 -

×

Elliottwave - Introduction to Spotting Elliott Wave Trading Opportunities

1 × $25.00

Elliottwave - Introduction to Spotting Elliott Wave Trading Opportunities

1 × $25.00 -

×

Best Seller Publishing from Rob Kosberg

3 × $87.00

Best Seller Publishing from Rob Kosberg

3 × $87.00 -

×

Salzedo's Exercises for Harp: the Daily Dozen and the Conditioning Exercises by Alice Giles

1 × $37.00

Salzedo's Exercises for Harp: the Daily Dozen and the Conditioning Exercises by Alice Giles

1 × $37.00 -

×

TONY CECCHINE – SNAP NO TAP – VOL.6 | Digital Download

1 × $29.00

TONY CECCHINE – SNAP NO TAP – VOL.6 | Digital Download

1 × $29.00 -

×

John La Tourrette - Spine Youth Enhancement and Thought-Form Installation

1 × $47.00

John La Tourrette - Spine Youth Enhancement and Thought-Form Installation

1 × $47.00 -

×

Healing Self: Going Beyond Acceptance to Self-Compassion by Richard C. Schwartz

1 × $17.00

Healing Self: Going Beyond Acceptance to Self-Compassion by Richard C. Schwartz

1 × $17.00 -

×

Brian Willie - Maps Lab

1 × $47.00

Brian Willie - Maps Lab

1 × $47.00 -

×

Kezia – Bundle Pack

1 × $87.00

Kezia – Bundle Pack

1 × $87.00 -

×

DigitalMarketer – Erin MacPherson – Beyond The Blog Workshop

1 × $32.00

DigitalMarketer – Erin MacPherson – Beyond The Blog Workshop

1 × $32.00 -

×

Alpha Male Series by Arash Dibazar

1 × $47.00

Alpha Male Series by Arash Dibazar

1 × $47.00 -

×

Badass Buddha by Tom Torero

1 × $29.90

Badass Buddha by Tom Torero

1 × $29.90 -

×

Market Essentials " Core, Swing, Options, Guerrilla, Trading Tactics" 2005 by Oliver Velez

1 × $88.00

Market Essentials " Core, Swing, Options, Guerrilla, Trading Tactics" 2005 by Oliver Velez

1 × $88.00 -

×

The Helper Healers - How to sell without selling

2 × $47.00

The Helper Healers - How to sell without selling

2 × $47.00 -

×

ReversionTE (Dec 2014)

1 × $85.00

ReversionTE (Dec 2014)

1 × $85.00 -

×

Larry Connors – Swing Trading College IX 2010

1 × $35.00

Larry Connors – Swing Trading College IX 2010

1 × $35.00 -

×

Super Achiever Coaching Program 18 - Week 6b-8, Fixes, and Monique Ga. by Stuart Lichtman

1 × $86.90

Super Achiever Coaching Program 18 - Week 6b-8, Fixes, and Monique Ga. by Stuart Lichtman

1 × $86.90 -

×

Wholesaling for Quick Cash Home Study Course

1 × $142.00

Wholesaling for Quick Cash Home Study Course

1 × $142.00 -

×

Innovations in Dementia Rehab from Jane Yakel

1 × $12.00

Innovations in Dementia Rehab from Jane Yakel

1 × $12.00 -

×

Gettingstartedwithpythonforquantfinance - Python for Quant Finance

1 × $199.00

Gettingstartedwithpythonforquantfinance - Python for Quant Finance

1 × $199.00 -

×

Raman – The Self Publishing Class

1 × $87.00

Raman – The Self Publishing Class

1 × $87.00 -

×

Niraj Naik - Renew Your Body & Reprogram Your Reality With SOMA Breathwork

1 × $95.00

Niraj Naik - Renew Your Body & Reprogram Your Reality With SOMA Breathwork

1 × $95.00 -

×

Arash Dibazar - The Man God

1 × $37.00

Arash Dibazar - The Man God

1 × $37.00 -

×

Jazz Guitar Improv Bundle by Marc-Andre Seguin

1 × $72.00

Jazz Guitar Improv Bundle by Marc-Andre Seguin

1 × $72.00 -

×

The Program’s Course – Online Home Study Course

1 × $55.00

The Program’s Course – Online Home Study Course

1 × $55.00 -

×

Iquim - Dr Debrah Zepf - Introduction to Aromatherapy Reupload

1 × $87.00

Iquim - Dr Debrah Zepf - Introduction to Aromatherapy Reupload

1 × $87.00 -

×

Aaaquants - AAAQuants Complete Trading-Bundle

1 × $239.00

Aaaquants - AAAQuants Complete Trading-Bundle

1 × $239.00 -

×

Jason Henderson - Breakthrough Email Swipe Files

2 × $147.00

Jason Henderson - Breakthrough Email Swipe Files

2 × $147.00 -

×

Email Inception Msatermind from Ben Adkins

1 × $57.00

Email Inception Msatermind from Ben Adkins

1 × $57.00 -

×

Digestion by Sound Healing Center

1 × $22.00

Digestion by Sound Healing Center

1 × $22.00 -

×

Anthony Robbins – Date with Destiny Australia 2002 Seminar Manual

1 × $15.00

Anthony Robbins – Date with Destiny Australia 2002 Seminar Manual

1 × $15.00 -

×

Ben Adkins – InstaClient Recipe

1 × $62.00

Ben Adkins – InstaClient Recipe

1 × $62.00 -

×

Marie Diamond - Feng Shui Fest 2016

1 × $42.00

Marie Diamond - Feng Shui Fest 2016

1 × $42.00 -

×

Anthony Robbins - Ultimate Edge 2018

2 × $12.00

Anthony Robbins - Ultimate Edge 2018

2 × $12.00 -

×

Paw Patrol Jet to the Rescue 2020 720p

1 × $12.00

Paw Patrol Jet to the Rescue 2020 720p

1 × $12.00 -

×

Growth Summit Online Conference from Eric Siu

1 × $32.00

Growth Summit Online Conference from Eric Siu

1 × $32.00 -

×

Trendfund.com – Scalping, Options, Advanced Options

1 × $37.00

Trendfund.com – Scalping, Options, Advanced Options

1 × $37.00 -

×

Rick Collingwood – Personal Life Motivation

1 × $17.00

Rick Collingwood – Personal Life Motivation

1 × $17.00 -

×

Micronics Zero-To-Hero Security Bootcamp

1 × $247.00

Micronics Zero-To-Hero Security Bootcamp

1 × $247.00 -

×

Aaron Ward - Instagram Masterminds 2.0

1 × $25.00

Aaron Ward - Instagram Masterminds 2.0

1 × $25.00 -

×

Dating Principles For Great Relationships by David Wygant

1 × $29.00

Dating Principles For Great Relationships by David Wygant

1 × $29.00 -

×

Hector E. Garcia - Guiding Personal Source - An Intuitive Healing Path to Clarity, Balance and Empowerment

1 × $19.00

Hector E. Garcia - Guiding Personal Source - An Intuitive Healing Path to Clarity, Balance and Empowerment

1 × $19.00 -

×

Neil Melanson - Ground Marshall Leglocks

1 × $27.00

Neil Melanson - Ground Marshall Leglocks

1 × $27.00 -

×

Ben Adkins – The Done For You Website Subscription Model

1 × $127.00

Ben Adkins – The Done For You Website Subscription Model

1 × $127.00 -

×

Ken Wilber – Full Spectrum Mindfulness

1 × $47.00

Ken Wilber – Full Spectrum Mindfulness

1 × $47.00 -

×

Matt D'Aquino Grappling Games for Kids

1 × $19.00

Matt D'Aquino Grappling Games for Kids

1 × $19.00 -

×

ConversionXL – Curt Maly – Become Great At Facebook Ads

1 × $42.00

ConversionXL – Curt Maly – Become Great At Facebook Ads

1 × $42.00 -

×

Dylan Werner - Flying Vinyasa Yoga Class

2 × $29.00

Dylan Werner - Flying Vinyasa Yoga Class

2 × $29.00 -

×

Figure Elancer from Secrets Of A Six

1 × $47.00

Figure Elancer from Secrets Of A Six

1 × $47.00 -

×

Deepak Chopra - What are You Hungry For?

1 × $12.00

Deepak Chopra - What are You Hungry For?

1 × $12.00 -

×

Vertexinvesting – Vertex Investing Course

1 × $27.00

Vertexinvesting – Vertex Investing Course

1 × $27.00 -

×

Empowering The Knight Within from John Cooper

1 × $69.00

Empowering The Knight Within from John Cooper

1 × $69.00 -

×

Facebook Agency Revolution from Jonny West

1 × $82.00

Facebook Agency Revolution from Jonny West

1 × $82.00 -

×

The Sex Sutras of 9th Limb Yoga from Arash Dibazar, Yogi Chris

1 × $45.00

The Sex Sutras of 9th Limb Yoga from Arash Dibazar, Yogi Chris

1 × $45.00 -

×

Pristine – Greg Capra – Intra-Day Trading Tactics

1 × $25.00

Pristine – Greg Capra – Intra-Day Trading Tactics

1 × $25.00 -

×

MetaStock Encyclopedia of Formulas

1 × $149.00

MetaStock Encyclopedia of Formulas

1 × $149.00 -

×

Mike Reed – Read the Greed-Live! Course

1 × $39.00

Mike Reed – Read the Greed-Live! Course

1 × $39.00 -

×

High Ticket Shortcuts from Eric Louviere

1 × $122.00

High Ticket Shortcuts from Eric Louviere

1 × $122.00 -

×

ConversionXL, Alexa Hubley - Project Management For Marketing project management

1 × $142.00

ConversionXL, Alexa Hubley - Project Management For Marketing project management

1 × $142.00 -

×

The Market Research Blueprint from Brittany Lynch

1 × $82.00

The Market Research Blueprint from Brittany Lynch

1 × $82.00 -

×

The Online Musician 3.0 by Leah McHenry

1 × $199.00

The Online Musician 3.0 by Leah McHenry

1 × $199.00 -

×

V.A. - The Essential Oils Revolution Summit

1 × $37.00

V.A. - The Essential Oils Revolution Summit

1 × $37.00 -

×

Football Dutching Systems by Chris Williams

1 × $22.00

Football Dutching Systems by Chris Williams

1 × $22.00 -

×

Ron Legrand – Commercial Property Bootcamp

1 × $145.00

Ron Legrand – Commercial Property Bootcamp

1 × $145.00 -

×

Ultimate Language Pattern Collection by Ross Jeffries

1 × $47.00

Ultimate Language Pattern Collection by Ross Jeffries

1 × $47.00 -

×

Daryl Guppy – Trend Trading

1 × $12.00

Daryl Guppy – Trend Trading

1 × $12.00 -

×

Trend Trading My Way 2010 by Markay Latimer

1 × $188.00

Trend Trading My Way 2010 by Markay Latimer

1 × $188.00

Subtotal: $29,428.40